ChatGPT, an OpenAI (backed by MSFT) chatbot, was released in November 2022, and quickly gained popularity for its human-like answering capabilities across many domains of knowledge. Consequently, OpenAI was reportedly valued at $29 billion post the release of ChatGPT. ChatGPT is built on Transformer, a neural network architecture that Google Research invented and open-sourced in 2017. Google also introduced its own language model Bard (powered by LaMDA, a ChatGPT equivalent) built on the same Transformer architecture with capabilities similar to ChatGPT. The Internet is now replete with examples of how ChatGPT can respond like a human, write poetry to computer code, and everything in between. In Part – I of this series of articles we discussed the consumer side of ChatGPT and its competitive positioning while in this article we look at the customer service (enterprise side) use cases of ChatGPT & Bard.

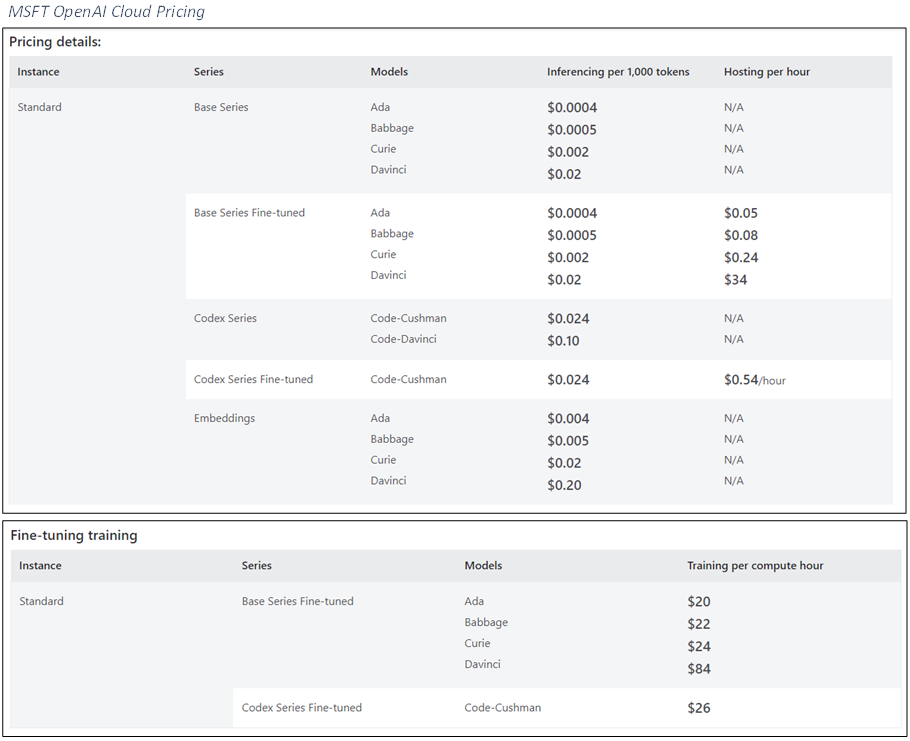

While most conversations revolve around how consumers are using ChatGPT to write articles, computer code, etc. MSFT & GOOGL are busy disrupting the Customer Service industry with ChatGPT & Bard. This is the first revenue-generating use case for these AI models. MSFT is about six months ahead of GOOGL and based on our industry checks, can’t hire enough engineers and sales representatives to help Fortune five hundred companies move their Customer Service to ChatGPT-trained models. As you can see from the table below, MSFT has already published a pricing chart for the OpenAI model’s Inference cost as well as Training costs. The training cost is generally a one-time upfront cost to train, for example, American Airlines Customer Service ChatGPT Customer Service model with 30,000 Customer Service call transcripts and company documents. Inference is the ongoing costs incurred by a company to use the ChatGPT-based model on a daily basis in a production environment once the model is trained. Other use cases include document summarization, call center transcript summarization, or taking call center transcripts and writing emails to send back to customers. The Global Call Center Industry TAM in CY22 is estimated at $350B. All of these use cases on the enterprise (customer service) side are generating revenue streams for both MSFT & GOOGL starting this quarter while we await better models and monetization use cases on the consumer side (poetry, articles, code writing).

For MSFT & Google, the timing couldn’t get better. Just when most of the tech industry is laying off staff, they have this huge demand from enterprises that want to move to ChatGPT. Both MSFT and Google were estimating a slowdown in Cloud Service revenue growth in CY23. This new revenue stream is likely to help them reverse some of that slower growth in CY23 and once inference revenues start in CY24 after 3-6 months of training period for these models, it could significantly improve the growth profile of their Cloud businesses. CY23 is likely to be only training revenues which may not be significant but once they get into production (inference) in Q4CY23 and CY24, post-training, the increase in revenues will be about 20x of training revenues and inference revenues are annuities that grow with model usage.

Conclusion: Based on our discussion with industry experts and from the pricing charts above, MSFT has a head start in monetizing ChatGPT for enterprises compared to Google’s Bard (still in testing mode). Moreover, MSFT has a very strong enterprise sales force covering almost all large enterprises for Office and Windows sales which makes the ChatGPT customer service collaboration quick and easy. So, round one of ChatGPT vs. Bard goes to MSFT, and from a revenue perspective MSFT will be the frontrunner for the next few quarters. Eventually, both MSFT & Google will benefit since just the Global Call Center market in CY22 was $350B which is a new TAM for both of them. The larger prize though, on the consumer search side, is still up for grabs where Google has a monopoly. Google commands a 93% share in the consumer search market while MSFT is at 3%, however, the risk to Google is asymmetric. Google has everything to lose and nothing to gain while MSFT has nothing to lose and any gains are incremental.

Don’t miss an update, subscribe to our LinkedIn Newsletter (https://lnkd.in/d3A7mpVP)

or join our open to all Telegram group for daily updates at: https://t.me/bayfortcapital

#stockmarket #stockmarketnews #sp500 #stocks #MSFT #GOOGL #chatgpt #Bard

Link to Part – I in this series of articles.