Much of Microsoft’s total addressable market (TAM) growth depends on ChatGPT’s integration into its product suite and the use of exclusivity to operate ChatGPT on its cloud infrastructure as a differentiator, enabling Microsoft to gain cloud infrastructure market share from Amazon and Google. Before the introduction of ChatGPT, the cloud infrastructure industry was becoming somewhat commoditized, with the Hyperscalers mostly competing based on price and efficiency. However, now anyone who wants to use ChatGPT has to use Microsoft’s Cloud Infrastructure, giving Microsoft a competitive advantage. Additionally, as the industry moves beyond basic Cloud Infrastructure to more software services such as Saas and Paas, ChatGPT provides Microsoft with a head start in these segments.

Currently, MSFT is winning the cloud services sector with market share gains, with Google coming in at a close second. On the other hand, Amazon is pursuing a different strategy by not offering its own ChatGPT model but instead offering to be a model-neutral cloud infrastructure service provider that allows other models to operate on its cloud. In the initial years where ChatGPT and Bard are likely to have higher market share, Amazon will be at a disadvantage since these two models must be run exclusively on MSFT and Google Cloud respectively while they also allow other models to run on their Cloud.

As the industry approaches 85% of global IT infrastructure on the cloud by the end of CY 2024, the next round will belong to companies that can offer the next level of SaaS & PaaS services such as data processing, analytics, and other tools. The competition among the three major players (MSFT, Amazon, and Google) is fierce to win the next round, with MSFT having a good chance of winning due to its strength in the enterprise space with Dynamics and its ChatGPT-related AI investments.

The race is on for the Hyperscalers to build software services beyond basic cloud infrastructure hosting, such as data warehousing software, databases, CRM software, and more. It is important to note that while all companies can use ChatGPT-4 APIs to provide AI applications, only MSFT has access to ChatGPT-4 source code to customize the base model for specific use cases. With ChatGPT, MSFT is introducing advanced AI features in SaaS & PaaS software services as a differentiator and is expected to gain market share. For e.g previously, competition in data warehousing was based on providing commoditized features, keeping up with industry leaders such as Snowflake, and competing more on price and efficiency, but with MSFT’s access to ChatGPT-4 source code, the company can compete on advanced AI features. This access provides MSFT with a significant advantage and fundamentally changes the competitive landscape in cloud infrastructure, SaaS, and PaaS segments.

Overall, ChatGPT provides Microsoft with a unique competitive advantage in the Cloud Infrastructure market and sets it apart from its competitors. As the industry continues to evolve, Microsoft’s access to ChatGPT-4 source code will allow it to stay ahead of the game and gain market share in the Saas and Paas segments.

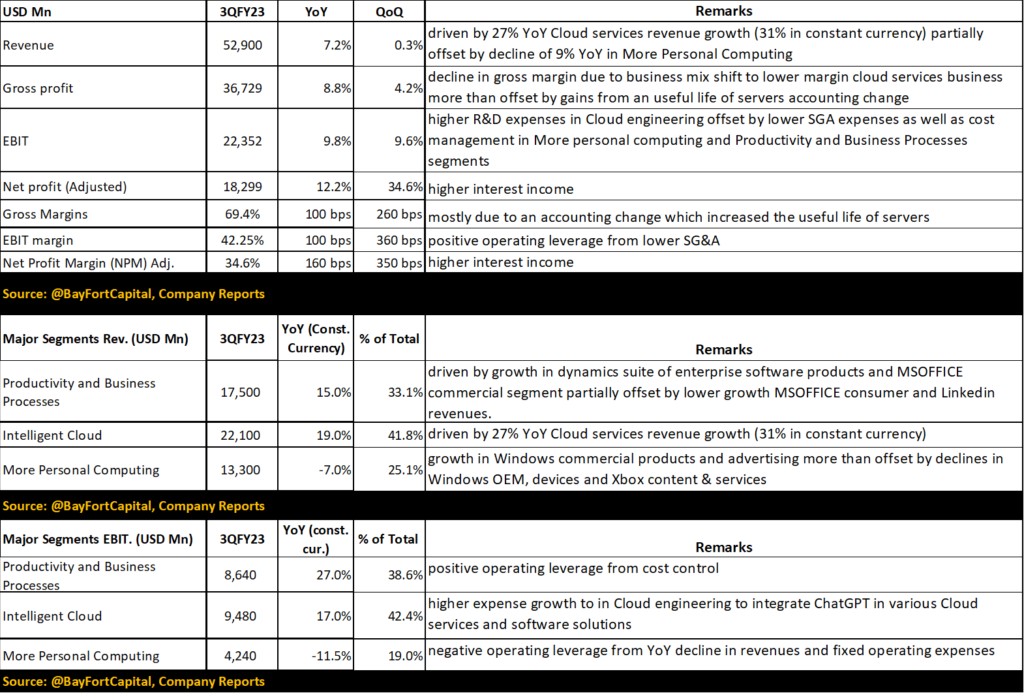

Revenues:

As Q1CY23 began, Microsoft’s Cloud segment, which was a major driver of growth, faced the prospect of slower growth in CY23 as customers looked to optimize Cloud spending. This trend was expected to affect all three Cloud Hyperscalers, including Amazon, Microsoft, and Google. With Windows revenue growth declining and MSOffice also expected to slow down as enterprises reduce hiring, Cloud services remained the only major growth leg for Microsoft, even prior to the pandemic.

However, in Q1CY23 (Q3FY23, June end Fiscal year-end), ChatGPT changed everything for Microsoft. Thousands of enterprise customers signed up to use Microsoft’s AI/ML models (ChatGPT) on its Cloud, which is mandatory for using the ChatGPT series of AI models. As a result, Amazon and Google Cloud customers who want to use ChatGPT are now required to use Microsoft’s Cloud, which is likely to help Microsoft gain market share in the cloud business and improve margins by eliminating the need to compete on price in the highly competitive Cloud infrastructure business.

Furthermore, the integration of AI technology into MS Office and Windows creates a compelling reason for current users to upgrade to the next version, resulting in increased average revenue per user (ARPU) for Microsoft. Considering these advancements, we anticipate an estimated compound annual growth rate (CAGR) of 11% for Microsoft’s revenue between FY23-25 (June-end Fiscal Year).

EBIT:

MSFT’s ChatGPT exclusivity helps in a commoditizing cloud market by providing a margin cushion, while significant AI-related feature enhancements in MS Office and Windows result in higher ARPU. MSFT has historically demonstrated high operating leverage, as fixed expenses such as R&D and SG&A have remained steady as long as revenue growth is in the high single digits. In the near future, R&D expenses are likely to rise as MSFT incorporates ChatGPT into all of its software solutions, including MS Office, Windows, and Dynamics. Companies that invest in R&D during downturns tend to perform well after the downturn, as they have a significant lead over competitors who reduced R&D investments during the downturn. While other firms have reduced R&D expenses, MSFT’s Cloud operating expenses grew by 18% YoY in the previous quarter and are expected to grow at a rate of 18-20% YoY, as most of this spending is directed toward Cloud engineering to integrate ChatGPT with other MSFT products. We estimate a 15% CAGR EBIT for FY23-25 (fiscal year ending June).

EPS:

We est. 16% EPS CAGR for FY23-25 (June ending Fiscal Year)driven primarily by increased interest income from a large amount of cash on Microsoft’s balance sheet, as well as the impact of stock buybacks. If interest rates remain high in the coming quarters, the higher interest income from Microsoft’s $104 billion cash reserves could become a significant contributor to YoY earnings growth, given the expected total net income of $71 billion for FY23.

Valuation:

The stock trades at 26x CY24E earnings and a 3.25% adjusted CFO (TTM) yield. It screens as slightly expensive compared to its mega-cap tech peers and cheap compared to large-cap (not mega-cap) enterprise software peers.

Risks:

The recent surge in the value of MSFT stock can be attributed to the excitement surrounding ChatGPT and its potential integration into MSFT’s Cloud services, SaaS, PaaS software, and future versions of MS Office and Windows. The stock’s support could wane if Microsoft fails to produce significant revenues in the near term (NTM) despite its promising long-term vision. The market will give MSFT 6-12 months to show meaningful revenues from AI services beyond which the focus will shift to execution and how quickly they can ramp up revenues from AI. As AI revenue expectations are built into the stock price ahead of execution, we will monitor MSFT’s pace of execution to see if the valuation and market expectations from MSFT’s AI business are in sync with the ground reality (revenue generation) over the next few quarters. We are quite comfortable with MSFT’s execution in the Cloud services segment, however, user acceptance of AI upgrades to MS Office & Windows (58% of FY23E revenues) requires careful attention.